Disclaimer: This article is for informational purposes only about Seychelles IBC accounting requirements and does not constitute legal, tax, or accounting advice. Rules change. Your situation is specific. Always consult a qualified professional before taking action.

Contents

- Seychelles IBC Accounting Requirements 2026: What You Actually Owe

- I. Why Seychelles Is Still One of the Best IBC Jurisdictions in 2026

- II. Seychelles IBC Structure: What You Are Actually Forming

- III. Seychelles IBC Accounting Requirements: The Core Obligations

- IV. Economic Substance Rules: What Every IBC Owner Needs to Know

- V. Banking for Your Seychelles IBC in 2026

- VI. Tax Obligations in Your Home Country: The Part Most Founders Overlook

- VII. Seychelles IBC Annual Compliance Calendar

- VIII. Seychelles IBC Accounting Requirements Matrix: What Applies to Your Company

- IX. Common Questions About Seychelles IBC Accounting Rules

- X. Common Mistakes Violating Seychelles IBC Accounting Requirements

- XI. 2026 Seychelles IBC Accounting Requirements Compliance Checklist

Seychelles IBC Accounting Requirements 2026: What You Actually Owe

If you own a Seychelles IBC, or you are about to form one, do not rely on outdated guidance. Seychelles is now often compared with jurisdictions like BVI and Singapore, especially after the post-2022 compliance reforms. Since then, Seychelles has changed its accounting and compliance framework through the International Business Companies (Amendment) Act 2021 and later post-2022 changes. Ignoring those changes can lead to penalties.

Consequently, this guide explains the current accounting rules, the main compliance duties, and the practical issues many advisors leave out. Some founders also compare Seychelles with other offshore structures discussed on the Korporatio website.

One major change came in 2026. In fact, on 17 February 2026, the EU Council removed Seychelles from Annex II of its list of non-cooperative tax jurisdictions, after recognising its “Largely Compliant” rating on the OECD Exchange of Information on Request standard. As a result, this may improve how banks, EMIs, and counterparties view Seychelles IBCs in 2026. Overall, this guide explains what that means in practice.

Every Seychelles IBC must follow the same Seychelles accounting rules. However, your personal tax position is a separate issue: it depends on where you live, where you are tax resident, and where the business actually operates.

So, this guide shall cover both:

- what Seychelles requires from the company; and

- what your own country may still require from you.

────────────────────────────────────────

I. Why Seychelles Is Still One of the Best IBC Jurisdictions in 2026

Seychelles is often written off as a legacy jurisdiction. Nonetheless, that view is outdated. Over the last five years, Seychelles has quietly rebuilt its legal architecture, and the result is a jurisdiction that is cheaper than BVI, and more flexible than Singapore. Seychelles has spent the last several years rebuilding its compliance reputation.

- The 2026 credibility reset

Seychelles spent years dealing with reputational issues. In October 2023, it landed on the EU’s list of non-cooperative jurisdictions. This followed a Partially Compliant rating from the OECD Global Forum on Exchange of Information on Request. It hurt banking and trust. Some founders moved instead toward jurisdictions such as Wyoming or Panama during that period. Frankly, it also damaged Seychelles’ reputation with banks and service providers.

However, the response was not cosmetic. Seychelles rewrote its accounting record-keeping rules. It overhauled beneficial ownership reporting. It also updated its business tax regime to match EU substance expectations. Subsequently, the Global Forum granted a supplementary review. In February 2024, Seychelles moved from Annex I (blacklist) back to Annex II (watchlist). Finally, on 17 February 2026, the Council of the European Union removed Seychelles from Annex II entirely. The Council acknowledged Seychelles’ Largely Compliant rating on the international EOIR standard.

Separately, Seychelles is not on the FATF’s current list of jurisdictions under increased monitoring. Moreover, ESAAMLG has overseen its AML/CFT progress. FATF’s June 2023 follow-up report also upgraded five of its technical compliance ratings. In fact, these developments affect banking and compliance risk. While some banks may apply tighter internal scrutiny to grey-listed jurisdictions as a matter of risk policy, FATF itself does not call for automatic enhanced due diligence for jurisdictions under increased monitoring. FATF calls for a risk-based approach.

B. What makes Seychelles attractive for founders

Several features continue to attract founders to Seychelles structures. The same comparison often appears against structures in Belize and St. Vincent and the Grenadines. A Seychelles IBC is cheap to form. It is exempt from local tax on foreign-source income. It also needs only one director and one shareholder. They can be the same person. They can also be from any country and live anywhere. There is also no minimum paid-up capital requirement, meaning the company may be formed with nil paid-up capital. Additionally, a Seychelles IBC can be incorporated in four or five working days.

Privacy remains one advantage of the structure. In particular, the register of directors and register of members are held by the registered agent and the FSA. They are not kept in a public database. Similarly, beneficial ownership is filed with the Financial Intelligence Unit and is not public. As a result, competitors cannot easily search your name. Still, that does not mean anonymous. The rest of this guide explains the difference.

C. Who this guide is for

This is written for the founder who already owns or is seriously considering a Seychelles IBC. Your location does not change the Seychelles rules. Whether you live in Dubai, Lisbon, Lagos, São Paulo, Bangkok, or Sydney. The Seychelles IBC accounting requirements apply in the same way. However, your home-country tax situation may change. Tax rules depend on where you live, where you are tax resident, and where the business operates. For that reason, we cover both layers.

────────────────────────────────────────

II. Seychelles IBC Structure: What You Are Actually Forming

Before the accounting rules, you need to know what you are keeping books for.

A. The legal basis

A Seychelles IBC is formed under the International Business Companies Act 2016, as amended by the IBC (Amendment) Act 2021 and later updates. It is a private company limited by shares. However, the Act gives strong flexibility. A Seychelles IBC may have one director, one shareholder, no residency rule, no minimum paid-up capital, no duty to hold annual general meetings in Seychelles. Furthermore, directors can be individuals or corporate entities.

Specifically, the IBC must appoint and maintain a Seychelles-licensed registered agent. The agent is regulated by the Financial Services Authority. The agent files incorporation papers, holds statutory registers, and acts as the legal channel between the company and Seychelles authorities. A Seychelles IBC must maintain a licensed registered agent..

📌 Client note:

The registered agent plays a central compliance role. An IBC cannot operate lawfully without one.

B. What an IBC can and cannot do

An IBC is mainly built for business outside Seychelles. Under the International Business Companies Act 2016, an IBC must not carry on business in Seychelles, except in limited cases allowed by the Act. Those limited cases include keeping a Seychelles bank account, using local lawyers or accountants, keeping records in Seychelles, holding meetings in Seychelles, and signing contracts in Seychelles for business carried on outside Seychelles.

However, the rule is no longer as simple as “no Seychelles activity.” If an IBC earns assessable income in Seychelles, it must notify the Registrar within one month and file an annual return within one year, under section 361 of the IBC Act. That can also create tax and reporting duties.

An IBC also cannot offer regulated services without the right licence or legal permission. This includes banking, insurance, international corporate services, securities business, mutual fund business, gambling, and similar regulated work under section 5(2) of the IBC Act. In particular, crypto activity is now regulated in Seychelles under the Virtual Asset Service Providers Act 2024. This is stricter than the approach still seen in some traditional offshore jurisdictions.

C. The registers you need to understand

There are three registers, and they don’t work the same way:

- Register of Members (shareholders): This is the shareholder register. It is kept at the registered office in Seychelles. It is not filed with the Registrar and is not public.

- Register of Directors: This register is kept by the company and must be filed with the Registrar under section 152 of the IBC Act. Access is limited. Directors and members can inspect it under section 151 of the IBC Act, but it is not treated as a public ownership database.

- Register of Beneficial Owners: This register is kept at the registered office in Seychelles under the Beneficial Ownership Act 2020. The resident agent uploads the required beneficial ownership details to the Seychelles BO database. The Financial Intelligence Unit maintains that database under the Beneficial Ownership Act.

Subsequently, access to the FIU database is restricted. Competent authorities (FIU, FSA, law enforcement, Seychelles Revenue Commission) can see it. The general public cannot.

However, extractive companies are subject to a special public-inspection rule under the Beneficial Ownership Act.

────────────────────────────────────────

III. Seychelles IBC Accounting Requirements: The Core Obligations

This is the core of the article. The Seychelles IBC accounting rules sit in section 175 of the IBC Act 2016, as amended by the August 2021 Amendment Act. Here is what every IBC owner must do.

A. Keep Accounting Records in Seychelles

Every Seychelles IBC must keep accounting records at its registered office in Seychelles. Before 2022, records could be kept outside Seychelles if the company told its registered agent where they were held. However, that changed after the 2021 amendment to section 175.

“Accounting records” is a broad term. It covers documents linked to the company’s assets, liabilities, receipts, spending, sales, purchases, and other transactions. This includes bank statements, invoices, receipts, contracts, loan agreements, title documents, vouchers, ledgers, and any document that proves a transaction. Records must also be kept for at least seven years from the date of the relevant transaction or operation.

Records may be kept in paper or electronic form. Moreover, if the registered office keeps copies instead of originals, the company must tell the registered agent, in writing, where the original records are kept. The records do not have to be in English. Still, the Registrar may ask for an English or French translation if the documents are in another language. For that reason, English records are often easier in practice.

📌 Practical note:

Most registered agents accept a clean PDF pack in date order: bank statements, invoices issued, invoices received, and a simple general ledger or transaction export. The bi-annual lodging rule applies to accounting records and supporting documents, not a full audit pack. Clear, complete, and matched records help avoid delays during compliance checks.

B. The bi-annual lodging schedule

Here is the rule that catches many founders. Specifically, Seychelles IBC accounting rules require records to be sent to the registered office at least twice a year. The FSA’s Circular No. 9 of 2021 explains the timing.

- Accounting records for the first half of the year, from January to June, must be kept in Seychelles by the end of July of that year.

- Accounting records for the second half of the year, from July to December, must be kept in Seychelles by the end of January of the next year.

This rule comes from section 175 of the IBC Act and the FSA’s guidance. Importantly, the records are not filed with the Registrar. They are also not open to public inspection. In practice, they must sit at the registered office and be ready if the Registrar, FSA, or another competent authority asks to inspect them.

Furthermore, struck-off and dissolved companies must still comply with outstanding record obligations. Their outstanding records must still reach the registered office by the end of the next January or July deadline after strike-off, dissolution, or deregistration.

C. The Annual Financial Summary

This is the part many founders miss. In addition to bi-annual records, some IBCs must prepare an Annual Financial Summary within six months of their financial year-end. Specifically, the 2021 amendment to section 175 created two key categories.

- Large Company: an IBC that meets the annual turnover threshold for a “large business” under the Revenue Administration Act. Current commentary places this threshold at SCR 50,000,000, approximately USD 3.6 million, depending on exchange rates.

- Holding Company: an IBC with no trade or business operations of its own, but which holds interests in other companies or assets.

In other words, every Large Company and every non-large company other than a pure holding company must prepare an Annual Financial Summary. Small pure holding companies are exempt from the Summary, although they must still comply with the bi-annual accounting records requirement.

Notably, the Summary is not a public filing. It is kept at the registered office with the underlying records under section 175 of the IBC Act. Moreover, section 175 does not create a general audit duty for every IBC. However, a separate licence can change the result. For example, a licensed VASP must prepare annual audited financial statements under the Virtual Asset Service Providers Act 2024, and FSA guidance says those audited accounts must follow IFRS and be submitted within six months after year-end. For most founders, the Annual Financial Summary is best treated as a short financial picture of the company. Trusted commentary describes it as a condensed summary of the company’s financial position, and some service providers describe the usual format as an income statement plus balance sheet.

D. The nominee shareholder declaration

Additionally, the 2025 amendments introduced a nominee shareholder declaration rule. A nominee member must give the company a written declaration within 21 days of appointment. The declaration must confirm the nominee status and identify the nominator. If the nominator’s details change, the nominee must send a written notice and a new declaration within 21 days. The company must keep these records at its registered office in Seychelles for at least seven years after the person stops being a nominee member. If you use a nominee shareholder, make sure the declaration is in place. Notably, banks and EMIs may also ask about nominee use during onboarding or review.

E. Penalties for non-compliance

Sections 175(5) and 175(6) of the IBC Act impose penalties of up to USD 10,000. The company can be fined. A director who knowingly allows the breach can also be fined. Importantly, these penalties apply per breach, not per year. Miss two lodging deadlines and a Summary, and the financial exposure can become significant..

Besides the statutory fine, non-compliance can create secondary costs. These may include registered agent remediation fees, loss of good standing, bank questions, and EMI account closure risk.

For annual-fee non-payment, the current FSA process is stricter. If an IBC fails to pay its annual fee within 180 days of the due date, the Registrar may strike off and dissolve the company on the 181st day. Do not rely on the old assumption that a company can remain struck off for one year before dissolution.

What These Rules Usually Do NOT Require in the Typical Offshore IBC Structure

Even after the 2021 reforms, a Seychelles IBC that earns only foreign-source income and has no relevant substance activity still faces relatively light compliance requirements::

- No mandatory filing of accounts with the Seychelles Registrar. Under section 350 of the IBC Act, an IBC may file annual financial statements with the Registrar, but does not have to.

- Furthermore, no public disclosure of financial statements, unless the company chooses to file them. The accounting records and Annual Financial Summary are kept at the registered office under section 175.

- No general audit requirement under section 175. However, a separate licence, sector rule, or tax position can change this.

- Also, no annual Seychelles business tax return in the normal case where the IBC earns only foreign-source income, is not part of a multinational group, and has no Seychelles-source income. Seychelles follows a territorial tax model, so offshore entities face Seychelles tax liability only to the extent they have Seychelles-source income. However, the standard case changes if the IBC derives assessable income in Seychelles, carries on taxable activity in Seychelles, is part of a multinational group with income caught by the Business Tax Act rules, or fails an applicable substance test.

- Finally, no Seychelles VAT merely because the IBC earns foreign-source income. Seychelles does have VAT, but VAT applies to taxable supplies made by a taxable person in the course of an enterprise carried on in Seychelles, and to taxable imports. So foreign-source IBC activity normally sits outside that VAT trigger.

Overall, the framework remains lighter than many onshore compliance systems. The trade-off is the record-keeping discipline itself, which the 2021 amendment made non-negotiable.

────────────────────────────────────────

IV. Economic Substance Rules: What Every IBC Owner Needs to Know

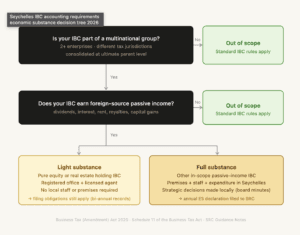

Substance is where most confusion starts. Notably, Seychelles substance rules are generally narrower than BVI’sthan BVI’s economic substance rules. In fact, most Seychelles IBCs are out of scope. Still, if your IBC is in scope, treat the rule seriously.

A. The legal basis

Seychelles substance rules come from the Business Tax (Amendment) Act 2020. The key rules came into force on 15 September 2021, together with Schedule 11 of the Business Tax Act and SRC guidance. Importantly, Seychelles made these changes to align its tax rules with OECD and EU standards on harmful tax practices.

B. Does this apply to you?

Two conditions must both be true before substance applies:

- First, your IBC must be part of a multinational group. That means a group with two or more enterprises that are tax resident in different jurisdictions. It also includes a case where one enterprise is resident in one country but taxed in another through a permanent establishment. The group test is based on accounting control and consolidation.

- Second, your IBC must earn foreign-source passive income in that tax year. This includes dividends, interest, rent, royalties, or capital gains.

For example, if your IBC is a single-owner trading or consulting company with no related-party consolidation, you are almost certainly out of scope. In contrast, if you hold IP inside a group with a parent that consolidates you, or you run a passive-income vehicle inside a family holding structure, the analysis becomes more fact-specific.

The Seychelles substance test mainly matters where an IBC is part of a multinational group and earns foreign-source passive income. However, this is not the whole tax analysis. Under the post-2021 business tax framework, if a Seychelles company is part of a multinational group, active income that is not attributable to a permanent establishment outside Seychelles may be taxed in Seychelles. Passive income may also be taxed in Seychelles if the company does not have adequate local substance.

📌 Client note:

Owning a Seychelles IBC does not automatically trigger the substance rules. First ask: “Am I part of a multinational group?” Then ask: “Did the IBC earn foreign passive income this year?” If the answer to either question is no, the standard Seychelles IBC accounting rules may still apply, but the economic substance test usually does not.

C. What “substance” means if you are in scope

Importantly, being in scope does not always require a full physical office in Victoria. The rules use two levels.

Light substance applies to pure equity holding companies and real estate holding companies. Specifically, these companies must meet their filing duties and have enough human resources and premises in Seychelles to hold and manage their investment assets.

Full substance applies to in-scope IBCs that are not pure holding or real estate holding companies. These companies must also:

- take key strategic decisions in Seychelles;

- manage and bear main risks in Seychelles;

- incur enough spending in Seychelles for the assets they buy, hold, or sell;

- use qualified staff or a properly supervised Seychelles-based service provider;

- keep proper records and self-assess the substance test in good faith.

Specifically, IP income is treated more strictly. Income from IP held in Seychelles is treated as Seychelles-source income unless it is qualifying income from a patent, or from a right that works like a patent. For that reason, if your structure licenses brand rights or know-how from a Seychelles IBC, founders should obtain specialist advice before restructuring IP assets.

D. Consequences of non-compliance

If an in-scope company fails the substance test, its foreign passive income can lose the foreign-source exemption. That income may then be treated as Seychelles-source income and taxed in Seychelles. The OECD 2026 review states that, where a Seychelles company is part of a multinational group and lacks adequate substance, its passive income is taxed in Seychelles.

The standard entity tax rates are 15% on the first SCR 1,000,000 (approximately USD 72,000, depending on exchange rates) of taxable income and 25% on the rest. The SRC may also require tax reporting where the new rules apply. Moreover, Seychelles participates in exchange of information on request, so tax-relevant information can be shared with foreign tax authorities through proper legal channels.

For EU-resident shareholders, this can also matter under local CFC rules. But the result depends on the shareholder’s home-country law.

⚠️ Warning: self-assessment regime

Seychelles operates as a self-assessment tax jurisdiction. The directors, not the SRC, must decide whether the IBC falls within the substance rules.

Getting this wrong can become expensive later. If any director, shareholder, or affiliate is linked to a multinational group, founders should obtain Seychelles tax advice before relying on the exemption.

────────────────────────────────────────

V. Banking for Your Seychelles IBC in 2026

Banking is the main friction point for offshore IBCs. The same issue affects companies formed in Panama,Belize, and other offshore jurisdictions. Seychelles is no exception. Still, the position is workable if your file tells a clear commercial purpose and transaction profile.

A. Local Seychelles banks

Local options include Absa Bank Seychelles, Mauritius Commercial Bank Seychelles, Nouvobanq, Seychelles Commercial Bank, Al Salam Bank Seychelles, Bank of Baroda and Bank of Ceylon. The Central Bank of Seychelles lists these commercial banks.

A local account is more realistic when the business has a clear Seychelles link, Indian Ocean link, or regional asset story. Do not apply with a vague “international business” profile. Seychelles banks must still check the client, ownership chain, business purpose, and account risk under basic FATF customer due diligence rules.

Expect proper KYC. For example, Absa Seychelles asks companies for formation papers, business address proof, valid ID for shareholders and directors, and proof of address dated within three months. MCB Seychelles asks for company papers, business address proof, financial documents, ID copies, and extra papers for non-residents, such as a bank reference and CV. Use the Absa Seychelles business account page and the MCB Seychelles company application form as practical guides.

B. Regional and offshore banks

Regional and offshore banks can still work. But treat this as a bank-by-bank review. Do not assume a Seychelles IBC will be accepted just because the company is legal and in good standing.

Mauritius can be a practical regional option when the business has a clear reason to bank there. Still, the bank will ask for details. For example, MCB’s business account form asks for the business model, sectors, counterparties, target markets, clients, and partners. See the MCB business account application form.

The same logic applies to Swiss, UAE, and Singapore banks. The issue is not only the Seychelles company. Banks usually review UBO residence, source of wealth, business activity, payment flow, counterparties, and the reason for banking in that country. Under FATF standards, banks must understand the purpose and nature of the business relationship.

C. Electronic Money Institutions (EMIs)

For many trading businesses, EMIs are useful. But support is not automatic. Each provider applies its own country rules, activity rules, UBO checks, and risk review.

Airwallex requires the business to be registered in an eligible country and to pass compliance checks. Dakota is also a popular option for many offshore companies, subject to approval.

3S Money publishes a Seychelles payments guide. Payoneer says its services remain subject to verification, eligibility, and service availability. See Payoneer’s guide on how businesses can get paid internationally.

D. What banks and EMIs will ask for

Expect KYC on every director, shareholder, and UBO. FATF standards require banks to identify and verify the customer and beneficial owner. Banks must also understand the account purpose and monitor the relationship based on risk.

Expect to provide:

- Certified passport copy.

- Proof of home address, often dated within the last three months.

- CV or professional profile, mainly for non-residents.

- Source of funds or source of wealth evidence.

- Business description.

- Expected transaction flows.

- Counterparty countries.

- Bank reference or proof of current business activity, where requested.

These documents form the core of the compliance review. Absa Seychelles and MCB Seychelles both publish document lists that show how normal these checks are for business accounts. See the Absa Seychelles business account page and the MCB Seychelles company application form.

The February 2026 EU delisting helps, but it does not guarantee account approval. It removes one formal EU tax-risk flag. Each bank or EMI still applies its own AML rules, tax-risk policy, and risk appetite. The EU Council confirmed that Seychelles was removed from Annex II after a positive Global Forum rating.

E. What Banks Usually Expect

Vague business descriptions get declined more easily. Specific ones give the bank something to assess. For example, if your IBC is a consultancy for African logistics clients, say that. Furthermore, name the industries, typical counterparties, expected monthly volumes, and payment corridors.

Banks expect a clear commercial rationale for the account.. MCB’s business account form asks for the mode of operations, sectors of activity, counterparties, target markets, clients, and partners. FATF customer due diligence rules also require banks to understand the purpose and nature of the relationship. Banks do not care that you formed in Seychelles for tax efficiency. They care that your transactions make business sense.

────────────────────────────────────────

VI. Tax Obligations in Your Home Country: The Part Most Founders Overlook

Your Seychelles IBC accounting requirements end with Seychelles. However, your tax duties may not. This is often the most misunderstood part of offshore structuring. Tax residence is set by each country’s own law, as the OECD explains. So here is a region-by-region walkthrough.

A. UAE residents

Since 1 June 2023, the UAE has applied federal corporate tax. The standard rate is 9% on taxable income above AED 375,000. A Qualifying Free Zone Person can still get a 0% rate on qualifying income, if it meets the legal conditions.

For UAE founders with a Seychelles IBC, the key questions are:

- First, is the Seychelles IBC tax-resident in the UAE through management and control? If you run the IBC from Dubai, make all key decisions there, and hold board meetings there, the UAE may treat the company as UAE tax-resident. The UAE Ministry of Finance states that corporate tax applies to foreign juridical persons that are effectively managed and controlled in the UAE.

- Second, does the IBC income reach you as dividends? UAE corporate tax law gives relief for certain dividends and foreign participation income through the participation exemption, subject to conditions.

- Finally, do UAE substance rules affect your UAE position? The old UAE economic substance regime is no longer the main issue for post-2022 periods. Instead, if you rely on QFZP status, the UAE corporate tax rules require the Free Zone Person to maintain adequate substance in the UAE. The FTA’s Free Zone Person guide explains those conditions.

Overall, UAE attribution rules are not the same as EU CFC rules. However, the management-and-control test is serious. Therefore, if you are a UAE resident and own a Seychelles IBC, you should obtain UAE tax advice before you rely on the structure. Many founders compare this setup against structures inSingapore orWyoming depending on their banking and tax priorities.

B. EU residents and ATAD CFC rules

If the shareholder is an EU corporate taxpayer, the ATAD CFC framework may matter. Article 7 of ATAD requires Member States to apply CFC rules where the control test and low-tax test are met. If the shareholder is an individual EU tax resident, ATAD itself is not the direct rule. The relevant question is the individual’s domestic tax law, including any personal CFC, anti-deferral, reporting, or anti-abuse rules.

Specifically, Article 7 uses two main tests:

- First, the taxpayer must hold more than 50% of the voting rights, capital, or profit rights, alone or with associated enterprises.

- Second, the foreign company must pay less than half the tax that would have applied under the taxpayer’s home-state corporate tax rules.

Notably, a Seychelles IBC with foreign-source passive income may pay 0% Seychelles tax on that income. That often satisfies the low-tax test. Consequently, if the shareholder also meets the control test, the home country may tax the income before any dividend is paid.

Member-state rules vary. France uses Article 209 B of the French Tax Code. Germany uses the Foreign Tax Act. Italy’s CFC regime is governed by Article 167 of the TUIR. Still, these regimes follow the same broad ATAD logic.

In short, if you are an EU-resident founder with control over a Seychelles IBC that earns passive income, the IBC may not remove the tax. It may only change the timing, paperwork, and audit risk. Founders should not assume the structure removes home-country tax exposure.

C. Australian residents

Australia’s CFC rules sit under Part X of the Income Tax Assessment Act 1936. If an Australian resident has a relevant interest in a Seychelles IBC, or if a small group of Australian residents controls it, Australian attribution rules may apply.

The active income test can give relief for real trading businesses. The ATO explains that this test is used to decide whether a CFC’s current-year profits are attributed to Australian residents. However, passive-income structures are harder to fit into that relief.

Therefore, for Australian residents, a Seychelles IBC is usually useful only where the business is genuinely active and the substance can be proved. Passive holding structures usually face closer tax review.

D. Rest of world: the common traps

For founders in other jurisdictions, the same issues keep appearing.

- Company tax residence. Many countries can treat a foreign company as locally tax-resident if it is managed from their territory. This is often called the “place of effective management” test. The OECD notes that tax residence depends on domestic law, so each country applies its own rule.

- CFC-style rules. Many major economies tax low-tax foreign companies owned or controlled by local residents. The OECD’s BEPS Action 3 report explains that CFC rules let countries tax income earned through foreign subsidiaries where set conditions are met. Japan has CFC rules, Mexico has REFIPRE rules, and South Africa has section 9D.

- Permanent establishment risk. If you run regular business from your home country in the IBC’s name, you may create a permanent establishment there. The OECD Model Tax Convention treats a permanent establishment as a fixed place of business through which the company’s business is carried on. If that happens, part of the IBC’s profit may become taxable in your home country.

E. CRS and Automatic Exchange of Information

Seychelles has implemented the Common Reporting Standard. The Seychelles Revenue Commission is the competent authority for international tax reporting. The SRC states that CRS submissions are due by 30 June each year.

CRS is simple in effect. A reporting financial institution collects account data, then reports it to the relevant tax authority. That data can include account balances, interest, dividends, and other reportable income. If the account is held in a CRS country, the information may reach the tax authority where the account holder is tax-resident. In short, CRS is how many tax authorities find undeclared offshore structures. Therefore, founders should assume tax authorities may receive this information.

Additionally, FATCA applies if a US person is involved. Seychelles signed a Model 1 FATCA agreement with the United States, and the official US Treasury FATCA agreement refers to account reporting duties for Seychelles financial institutions.

F. The practical takeaway

A Seychelles IBC can be useful for specific cases. Some founders also compare Seychelles with structures in Panama orBVI depending on their reporting and banking needs. These include holding structures outside high-tax jurisdictions, real businesses with activity outside the founder’s home country, and asset protection linked to real trade.

However, offshore structures no longer provide the secrecy many people assume. Founders who live in countries with CFC rules, management-and-control rules, or strong reporting systems may still face local tax and reporting duties. Tax authorities can often trace offshore companies through CRS, FATCA, bank reporting, and local filings. The real issue is whether the structure has a real legal and business purpose.

────────────────────────────────────────

VII. Seychelles IBC Annual Compliance Calendar

Here is the consolidated year-at-a-glance for a standard Seychelles IBC. Notably, exact dates depend on your financial year-end; for illustration, we assume a 31 December FY.

| Deadline | Obligation | Applies to | ||

|---|---|---|---|---|

| 31 January | Lodge H2 accounting records, covering July to December, at the registered office | All IBCs | ||

| Within 14 days of any UBO change | Update the beneficial ownership register and have the resident agent upload the change to the BO database | All IBCs | ||

| On anniversary of incorporation | Pay the annual government renewal fee and registered agent renewal. | All IBCs | ||

| 30 June | Prepare the Annual Financial Summary, due within 6 months after year-end, assuming a 31 December year-end | Large companies and non-large non-holding companies | ||

| 30 June | Submit CRS reporting through the relevant Seychelles financial institution | Seychelles-held accounts only | ||

| 30 June (FY dependent) | File the economic substance declaration with the SRC, where the IBC is in scope under the Business Tax Act substance rules | In-scope IBCs only | ||

| 31 July |

|

All IBCs | ||

| Ongoing | Keep KYC current with the registered agent, including identity and beneficial ownership records. AML-obliged persons must keep CDD records, including identity documents for customers and beneficial owners | All IBCs |

For most founders, the compliance cycle is relatively straightforward. Send your books in late January and late July. Keep beneficial ownership information current. Renew the company each year. Your registered agent should send reminders and templates. A reliable registered agent should provide regular reminders and compliance support.

────────────────────────────────────────

VIII. Seychelles IBC Accounting Requirements Matrix: What Applies to Your Company

You need precise answers regarding your compliance duties. The law dictates specific burdens based on your corporate activity. Consequently, generic offshore advice is often too broad for Seychelles compliance. We built the table below to isolate what your entity owes.

Locate your company type in the left column. Then, follow the row to understand your exact obligations under the current Seychelles IBC accounting requirements.

| Company Profile | Bi-annual Accounting Records | Annual Financial Summary | Economic Substance | BO/KYC File Impact | Practical Accounting Action |

| Standard trading or consulting IBC | Required | Required | Out of scope | 14-day update rule | Submit reconciled ledgers and receipts to the agent in January and July. |

| Small holding IBC (pure equity) | Required | Exempt | Light substance | 14-day update rule | Maintain and submit supporting records, including bank statements and portfolio documentation, on the bi-annual schedule. |

| Large company (>SCR 50m turnover) | Required | Required | Out of scope | 14-day update rule | File full bi-annual records and draft a formal annual summary. |

| Non-large, non-holding company | Required | Required | Out of scope | 14-day update rule | Submit bi-annual records and prepare the annual financial summary. |

| In-scope multinational group company | Required | Depends on size | Full substance | 14-day update rule | Submit records and file the annual SRC substance declaration. |

| Licensed VASP | Required | Audited IFRS | Full substance physical | Intense ongoing EDD | Submit audited IFRS accounts to the FSA within 6 months of year-end. |

| Dormant or struck-off IBC | Required | Exempt | Out of scope | 14-day update rule | Lodge zero-balance ledgers bi-annually to avoid strike-off penalties. |

Crypto accounting creates practical issues for many Seychelles IBCs. Under IFRS, crypto assets are generally not treated as cash. Consistent accounting treatment reduces compliance and audit risk.

Crypto Accounting Requirements for Seychelles IBCs

Many companies classify cryptocurrency under IAS 38 as intangible assets, although IAS 2 inventory treatment may apply depending on the business model. You only use the IAS 2 inventory classification if your core business involves selling tokens daily.

Companies should track crypto holdings separately from fiat balances. You record traditional cash in your standard bank reconciliation file. Conversely, digital tokens usually appear separately from fiat balances and may require impairment review.impairment testing. If the company holds only crypto assets, valuation methods and exchange rates become especially important at year-end.

Regulated virtual asset activity creates additional compliance obligations. If you operate an exchange, brokerage, or custodial wallet, the VASP Act 2024 applies. “The VASP regime may require licensing, local operational presence, and resident compliance arrangements. More importantly, a licensed VASP must submit fully audited IFRS accounts to the FSA within six months of its financial year-end.

Your registered agent needs clear data to file your bi-annual records. Do not send raw wallet addresses or blockchain hash links. You must provide exported exchange statements, chronological transaction logs, and clear fiat-value translation receipts. Specifically, your accountant should also keep documentation that proves the exact value of the asset at the moment of transfer.

────────────────────────────────────────

IX. Common Questions About Seychelles IBC Accounting Rules

Personal Expenses and Lifestyle Use

- Can my Seychelles IBC own a car and write it off?

No. Many tax authorities may treat personal use of a corporate vehicle as a taxable benefit in kind. Your home country will tax you personally on the vehicle’s full value. Personal use of a company vehicle may create tax consequences in your home jurisdiction. - Can the IBC pay for my rent or housing?

No. Mixing personal and company expenses can create tax and corporate-governance problems.. This can weaken the separation between personal and company finances.. You must extract capital via salary or dividends to pay residential rent.

- Can the IBC pay for my child’s school fees?

No. Private school tuition remains a Private school tuition is generally treated as a personal expense. Personal expenses paid through the company may create tax, accounting, or corporate-governance issues in the shareholder’s home jurisdiction - Can the IBC buy property?

Yes. Your company can legally hold real estate anywhere in the world. Furthermore, following the 2025 moratorium lift, your IBC can purchase residential property inside Seychelles designated areas. You must secure official government sanction before finalizing the local deed transfer. - Can I pay myself a salary from the IBC, and how does that interact with the accounting records?

Yes. You must draft a formal employment contract detailing your duties. The salary reduces your corporate profit as a standard business expense. Consequently, you must also report this income on your personal tax return where you reside.

Accounting Records and Compliance

- Do I need receipts for every transaction, or is a bank statement enough?

Bank statements alone are usually not enough. Section 175 expects companies to keep supporting records for transactions.. You must match every bank line item with a corresponding invoice, contract, or receipt. - My IBC is dormant this year. Do I still need to send records to the agent?

Yes. The law grants no reporting exemptions for dormant entities. You must submit a formal zero-balance ledger to your agent. Failure to comply may lead to penalties. - I have two IBCs. Do they each need separate records sent separately?

Yes. The registrar treats each company as a completely distinct legal entity. Therefore, you must maintain isolated bookkeeping ledgers for both. Transactions between companies should remain clearly separated.

Loans, Investments, and Trading Activity

- Can I use a director’s loan to extract tax-free cash?

- No. You must repay a director’s loan within a documented timeframe. If you fail to repay the funds, your home tax authority will reclassify the balance as a taxable dividend. Director loans can still create tax problems under your home country’s rules. In some cases, tax authorities may treat the loan as a dividend.

- Can I trade personal stocks through the IBC?

- Yes. Your company can hold brokerage accounts globally. Still, your home country’s Controlled Foreign Corporation (CFC) rules will likely apply. Your home-country tax rules may still apply to those trading profits.

────────────────────────────────────────

X. Common Mistakes Violating Seychelles IBC Accounting Requirements

Poor Record-Keeping

Many compliance problems come from poor record-keeping and missed deadlines.. Avoid these common compliance mistakes.

Registered Agent Mistake

Treating the registered agent as a mere mailbox is an error. Founders mistakenly assume they can simply hold records on their personal computers. Section 175 demands physical or digital lodgement at the Seychelles registered office. Breaches may expose the company and its directors to penalties of up to USD 10,000.

Missing the Bi-Annual Deadlines

Missing the bi-annual deadlines occurs when founders treat accounting as an annual chore. You must submit H1 records by July and H2 records by January. The FSA monitors registered-agent compliance, including record-keeping obligations. Set calendar alerts to enforce these fixed deadlines.

Tax Exemption Does Not Remove Accounting Duties

Confusing “no Seychelles tax return” with “no accounting obligation” affects many businesses. Under Seychelles’ territorial tax system, foreign-source income is generally outside Seychelles taxation. However, the record-keeping mandate applies universally to every incorporated entity. Tax exemption does not remove the accounting obligations.

Small Holding Company Confusion

Founders often confuse their exemption from the Annual Financial Summary with an exemption from record-keeping entirely. Small holding companies do skip the formal summary requirement. Yet, they must still lodge their bank statements and ledgers twice a year. Verify your exact entity classification before skipping any filings.

Crypto Record Keeping Problems

Poor crypto record-keeping often leads to banking and compliance problems. Sending an agent a raw wallet address often creates AML and compliance concerns. You must translate every digital transfer into fiat equivalents at the time of execution. Registered agents may pause the review process until you provide compliant, reconciled data.

Nominee Shareholder Declarations

Failing to keep nominee shareholder declarations on file triggers the 2025 amendment penalties. Nominees possess 21 days to submit a formal declaration revealing the ultimate owner’s identity. Ignoring this requirement may lead to penalties under the amended rules. You must execute this paperwork upon formation.

Disorganized Financial Records

Sending disorganized or unmatched records creates record-keeping gaps. Dumping raw receipts into a zip file often delays the compliance review process. You must logically match every invoice to its corresponding bank ledger line. Organized records make compliance reviews easier and reduce follow-up requests.

────────────────────────────────────────

XI. 2026 Seychelles IBC Accounting Requirements Compliance Checklist

Missing deadlines can lead to penalties and compliance problems. Use this checklist to track the main compliance deadlines.

January Actions

- Submit H2 accounting records (covering July–December) to your registered agent by January 31.

- Reconcile all end-of-year bank statements against issued invoices.

July Actions

- Submit H1 accounting records (covering January–June) to your registered agent by July 31.

- Verify all crypto asset valuations match the mid-year exchange rates.

Annual (Anniversary of Incorporation)

- Pay the government renewal fee to maintain active status.

- Renew your registered agent and registered office agreements.

Ownership or Control Changes (14 Days)

- Notify your registered agent of any new directors or shareholders.

- Update the internal Register of Members.

- Ensure the agent updates the confidential FIU beneficial ownership database.

Nominee Appointment Deadline (21 Days)

- Lodge the formal nominee shareholder declaration.

- Record the ultimate nominator’s full identity details in the corporate register.

Financial Year-End Requirements (6 Months)

- Prepare the Annual Financial Summary (if you operate a large or non-holding company).

- Submit fully audited IFRS accounts to the FSA (if you hold a VASP license).4

Ongoing Actions

- Maintain up-to-date KYC documents for all controllers.

- Preserve all transaction receipts, contracts, and crypto logs for seven years.

For a deeper analysis of Seychelles structures, visit the Seychelles section on theKorporatio website. Founders comparing Seychelles with other offshore structures can also review theBVI,Belize, and Panama sections on the Korporatio website. The site also contains additional material on banking, compliance, and offshore structures. Review the banking requirements before applying for accounts, and seek professional advice before building your compliance structure.

Disclaimer: This article is for informational purposes only about Seychelles IBC accounting requirements and does not constitute legal, tax, or accounting advice. Rules change. Your situation is specific. Always consult a qualified professional before taking action.

Accounting requirements for Belize LLC and IBC

Accounting requirements for Belize LLC.

0 Comments31 Minutes

Why Choose Seychelles?

Dynamic, cost-effective and versatile. Learn more why set up a company here!

0 Comments10 Minutes

Wyoming LLC Tax and Accounting Requirements for U.S. Citizens in 2026

Wyoming accounting requirements for LLCs for US residents.

0 Comments61 Minutes